Predicting Stock Prices with Monte Carlo Simulations

Introduction

In finance, decisions are rarely about a single “forecast” price: they are about ranges, tail risk, and how wrong simple models can be. This article walks through a Monte Carlo path simulation in Python: we estimate drift and volatility from historical closes, simulate many future price paths (a geometric Brownian–style discrete step), and summarize the result as a distribution—the right object for risk-style questions (bands, percentiles, coverage against a hold-out period).

Markov chain Monte Carlo (MCMC), as in Landauskas and Valakevičius’s paper on stock price modelling, is a different tool: it draws samples from a distribution that need not be a simple Gaussian—for example one built from a kernel density estimate of observed prices—whereas the code below assumes lognormal shocks from estimated drift and volatility. A practical workflow is MCMC (or other inference) for the law of the data, then forward Monte Carlo for multi-step scenarios. This post implements the forward GBM-style step explicitly; see the references and the linked work-in-progress below if you want to push toward paper-style MCMC.

Step 1: Setting Up the Environment

To start, we need to install the necessary Python libraries. These libraries include pandas, numpy, httpx, backtesting, pandas_ta, matplotlib, scipy, rich, and others. Here’s how to install them:

import pandas as pd

import numpy as np

from datetime import datetime

import concurrent.futures

import warnings

from rich.progress import track

from backtesting import Backtest, Strategy

import pandas_ta as ta

import matplotlib.pyplot as plt

from scipy.stats import norm

import httpx

warnings.filterwarnings(“ignore”)

Step 2: Defining Utility Functions

We need functions to fetch historical stock prices and crypto prices from APIs:

def make_api_request(api_endpoint, params):

with httpx.Client() as client:

# Make the GET request to the API

response = client.get(api_endpoint, params=params)

if response.status_code == 200:

return response.json()

print(“Error: Failed to retrieve data from API”)

return None

def get_historical_price_full_crypto(symbol):

api_endpoint = f"{BASE_URL_FMP}/historical-price-full/crypto/{symbol}"

params = {“apikey”: FMP_API_KEY}

return make_api_request(api_endpoint, params)

def get_historical_price_full_stock(symbol):

api_endpoint = f"{BASE_URL_FMP}/historical-price-full/{symbol}"

params = {“apikey”: FMP_API_KEY}

return make\_api\_request(api\_endpoint, params)

def get_SP500():

api_endpoint = “https://en.wikipedia.org/wiki/List_of_S%26P_500_companies”

data = pd.read_html(api_endpoint)

return list(data[0][‘Symbol’])

def get_all_crypto():

return [

“BTCUSD”, “ETHUSD”, “LTCUSD”, “BCHUSD”, “XRPUSD”, “EOSUSD”,

“XLMUSD”, “TRXUSD”, “ETCUSD”, “DASHUSD”, “ZECUSD”, “XTZUSD”,

“XMRUSD”, “ADAUSD”, “NEOUSD”, “XEMUSD”, “VETUSD”, “DOGEUSD”,

“OMGUSD”, “ZRXUSD”, “BATUSD”, “USDTUSD”, “LINKUSD”, “BTTUSD”,

“BNBUSD”, “ONTUSD”, “QTUMUSD”, “ALGOUSD”, “ZILUSD”, “ICXUSD”,

“KNCUSD”, “ZENUSD”, “THETAUSD”, “IOSTUSD”, “ATOMUSD”, “MKRUSD”,

“COMPUSD”, “YFIUSD”, “SUSHIUSD”, “SNXUSD”, “UMAUSD”, “BALUSD”,

“AAVEUSD”, “UNIUSD”, “RENBTCUSD”, “RENUSD”, “CRVUSD”, “SXPUSD”,

“KSMUSD”, “OXTUSD”, “DGBUSD”, “LRCUSD”, “WAVESUSD”, “NMRUSD”,

“STORJUSD”, “KAVAUSD”, “RLCUSD”, “BANDUSD”, “SCUSD”, “ENJUSD”,

]

def get_financial_statements_lists():

api_endpoint = f"{BASE_URL_FMP}/financial-statement-symbol-lists"

params = {“apikey”: FMP_API_KEY}

return make_api_request(api_endpoint, params)

Step 3: Splitting Data into Training and Testing Sets

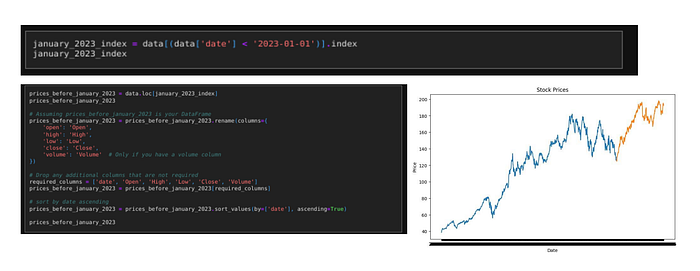

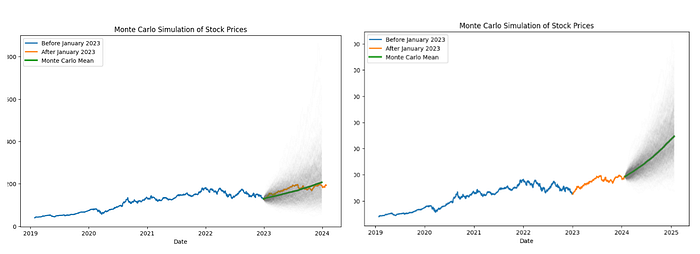

Next, we’ll fetch the historical stock prices for a given symbol and split the data into training and testing sets. We keep two frames: before January 2023 (used to estimate the model and run simulations) and from January 2023 onward (hold-out for comparing simulated ranges to realized prices).

stock_symbol = “AAPL”

stock_prices = get_historical_price_full_stock(stock_symbol)

data = pd.DataFrame(stock_prices[‘historical’])

def prepare_price_frame(df):

df = df.rename(columns={

‘open’: ‘Open’,

‘high’: ‘High’,

’low’: ‘Low’,

‘close’: ‘Close’,

‘volume’: ‘Volume’,

})

required_columns = [‘date’, ‘Open’, ‘High’, ‘Low’, ‘Close’, ‘Volume’]

return df[required_columns].sort_values(by=[‘date’], ascending=True).reset_index(drop=True)

prices_before_january_2023 = prepare_price_frame(data[data[‘date’] < ‘2023-01-01’])

prices_after_january_2023 = prepare_price_frame(data[data[‘date’] >= ‘2023-01-01’])

plt.figure(figsize=(10, 6))

plt.title(‘Stock Prices’)

plt.xlabel(‘Date’)

plt.ylabel(‘Price’)

plt.plot(prices_before_january_2023[‘date’], prices_before_january_2023[‘Close’], label=‘Train (before Jan 2023)’)

plt.plot(prices_after_january_2023[‘date’], prices_after_january_2023[‘Close’], label=‘Hold-out (from Jan 2023)’)

plt.legend()

plt.show()

Press enter or click to view image in full size

Press enter or click to view image in full size

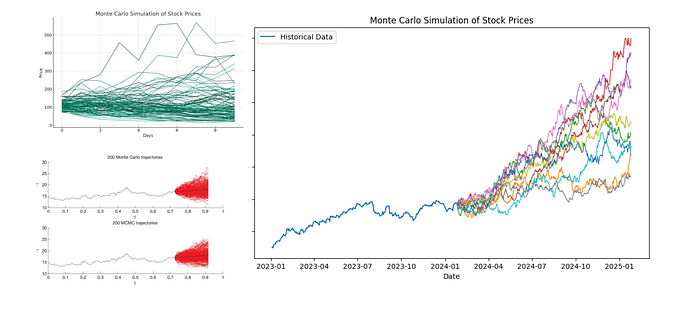

Step 4: Monte Carlo Simulation (Forward Paths and Risk Bands)

The function below is Monte Carlo simulation of a constant-parameter model: we estimate mean and variance of log returns on the training window, build a daily drift and volatility, then draw many independent Gaussian shocks and propagate price forward. That is not MCMC; there is no Markov chain sampling a posterior here. It is the kind of forward scenario engine you might run after inference. By contrast, Landauskas and Valakevičius (Intellectual Economics, 2011) use MCMC to sample from a distribution shaped by a kernel density estimate of prices (piecewise-linear proposals)—a way to stay close to the empirical law of the data with few parametric assumptions. Our GBM shortcut is simpler; the paper is the reference when you want the data-driven sampling step.

For a work-in-progress that extends this line of thought (batch experiments, richer risk views, and moving closer to paper-style MCMC), see this LinkedIn experiment (WIP).

The useful outputs for risk are distributions: percentiles of terminal price, prediction-style bands (for example 5th–95th percentile paths), and coverage checks against a hold-out (did realized prices sit where the simulated mass was?).

def monte_carlo_simulation(data, days, iterations):

if isinstance(data, pd.Series):

data = data.to_numpy()

if not isinstance(data, np.ndarray):

raise TypeError(“Data must be a numpy array or pandas Series”)

log\_returns = np.log(data\[1:\] / data\[:-1\])

mean = np.mean(log\_returns)

variance = np.var(log\_returns)

drift = mean - (0.5 \* variance)

daily\_volatility = np.std(log\_returns)

future\_prices = np.zeros((days, iterations))

current\_price = data\[-1\]

for t in range(days):

shocks = drift + daily\_volatility \* norm.ppf(np.random.rand(iterations))

future\_prices\[t\] = current\_price \* np.exp(shocks)

current\_price = future\_prices\[t\]

return future\_prices

Press enter or click to view image in full size

Press enter or click to view image in full size

Visualisation

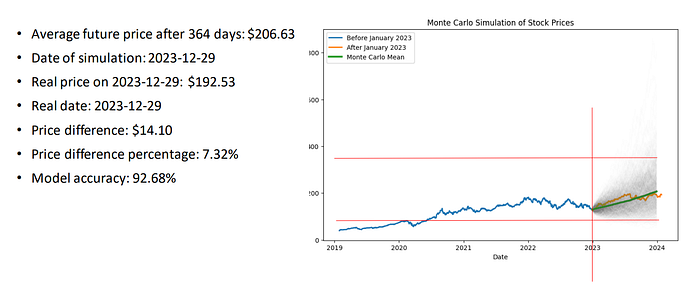

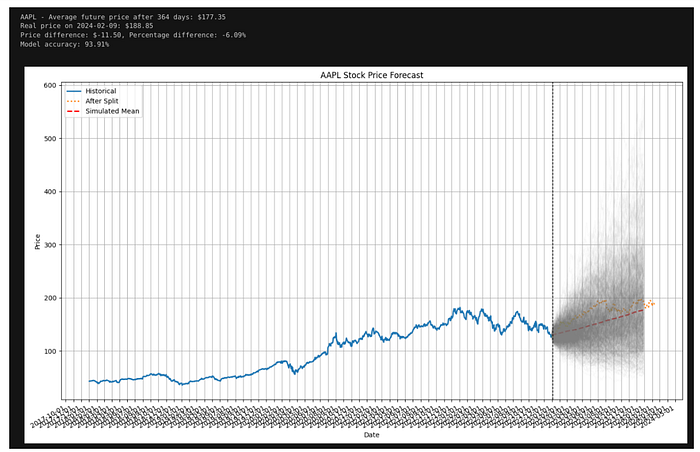

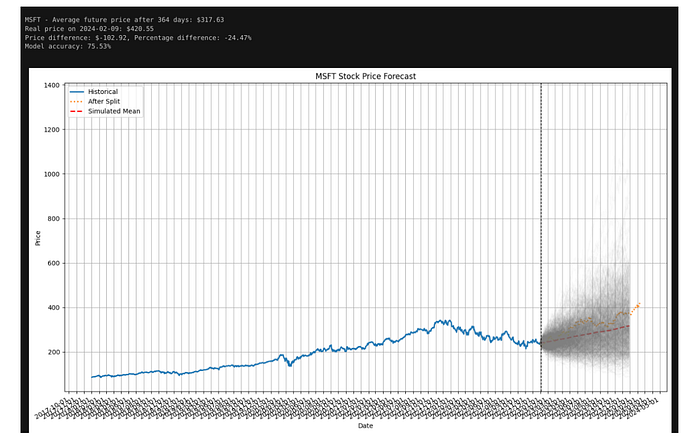

simulation_days = 364

mc_iterations = 1000

mc_prices = monte_carlo_simulation(prices_before_january_2023[‘Close’], simulation_days, mc_iterations)

last_train_close = prices_before_january_2023[‘Close’].iloc[-1]

last_close_price = np.full((1, mc_iterations), last_train_close)

mc_prices_combined = np.concatenate((last_close_price, mc_prices), axis=0)

last_date = prices_before_january_2023[‘date’].iloc[-1]

simulated_dates = pd.date_range(start=last_date, periods=simulation_days + 1)

# Percentiles across paths at each future step (risk band)

p05 = np.percentile(mc_prices_combined, 5, axis=1)

p50 = np.percentile(mc_prices_combined, 50, axis=1)

p95 = np.percentile(mc_prices_combined, 95, axis=1)

mean_path = mc_prices_combined.mean(axis=1)

# Terminal distribution at the last simulated step (VaR-style summaries)

terminal_prices = mc_prices_combined[simulation_days, :]

mean_terminal_price = float(np.mean(terminal_prices))

q5, q50, q95 = np.percentile(terminal_prices, [5, 50, 95])

terminal_return = terminal_prices / last_train_close - 1.0

ret_q5, ret_q50, ret_q95 = np.percentile(terminal_return, [5, 50, 95])

horizon_idx = min(simulation_days, len(prices_after_january_2023) - 1)

real_price = float(prices_after_january_2023[‘Close’].iloc[horizon_idx])

real_date = prices_after_january_2023[‘date’].iloc[horizon_idx]

in_90_band = q5 <= real_price <= q95

print(f"Simulated horizon: {simulation_days} trading days after {last_date}")

print(f"Mean terminal price: ${mean_terminal_price:.2f}")

print(f"Terminal price percentiles (5 / 50 / 95): ${q5:.2f} / ${q50:.2f} / ${q95:.2f}")

print(f"Terminal simple return vs last train close — 5th / 50th / 95th %ile: {ret_q5*100:.2f}% / {ret_q50*100:.2f}% / {ret_q95*100:.2f}%")

print(f"Hold-out price at aligned step ({real_date}): ${real_price:.2f}")

print(f"Realized price inside simulated 5–95% band: {in_90_band}")

plt.figure(figsize=(10, 6))

for i in range(mc_iterations):

plt.plot(simulated_dates, mc_prices_combined[:, i], linewidth=0.5, color=‘gray’, alpha=0.02)

plt.fill_between(simulated_dates, p05, p95, alpha=0.25, label=‘5th–95th percentile band’)

plt.plot(simulated_dates, p50, label=‘Median path’, linewidth=2, color=‘C0’)

plt.plot(simulated_dates, mean_path, label=‘Mean path’, linewidth=2, linestyle=’–’, color=‘C1’)

plt.plot(pd.to_datetime(prices_before_january_2023[‘date’]), prices_before_january_2023[‘Close’], label=‘Train (before Jan 2023)’, linewidth=2, color=‘black’)

plt.plot(pd.to_datetime(prices_after_january_2023[‘date’]), prices_after_january_2023[‘Close’], label=‘Hold-out (from Jan 2023)’, linewidth=2, color=‘green’)

plt.axvline(pd.to_datetime(real_date), color=‘red’, linestyle=’:’, linewidth=1, alpha=0.8, label=‘Hold-out step aligned to horizon’)

plt.scatter([pd.to_datetime(real_date)], [real_price], color=‘red’, s=40, zorder=5, label=‘Realized (aligned)’)

plt.title(‘Monte Carlo Simulation of Stock Prices (with percentile band)’)

plt.xlabel(‘Date’)

plt.ylabel(‘Price’)

plt.legend(loc=‘upper left’, fontsize=8)

plt.show()

Press enter or click to view image in full size

Press enter or click to view image in full size

Press enter or click to view image in full size

Press enter or click to view image in full size

Conclusion

Forward Monte Carlo gives you a distribution of future prices under an assumed dynamics—ideal for percentile bands, tail behaviour, and coverage checks against data you held out. That is a different step from MCMC, which is about sampling from a flexible model of the data (as in Landauskas and Valakevičius’s KDE-driven approach) before or alongside forward simulation. A practical pipeline is: fit or sample the distribution that matches history, then push scenarios forward with Monte Carlo. Combined with strategy backtesting, you separate “how wide is model risk?” from “does a rule make money?”

Related exploratory code: AlgoETS/MarkokChainMonteCarlo (stratification / MCMC-oriented experiments).

Reference

- Landauskas, M. & Valakevičius, E. (2011). Modelling of Stock Prices by Markov Chain Monte Carlo Method — Intellectual Economics, Vol. 5 No. 2 (article page); PDF download.

- Semantic Scholar index for the same paper.

- Neural Networks in Finance: Markov Chain Monte Carlo (MCMC) and Stochastic Volatility Modeling

- Monte Carlo Simulation Basics

Originally published on Medium.